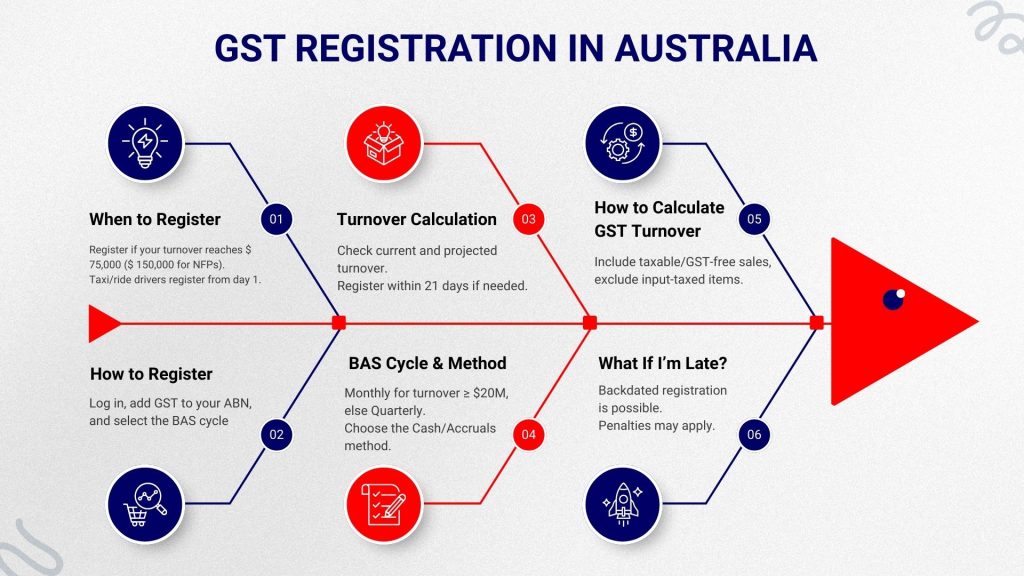

GST Registration in Australia: When to Register and How

If your GST turnover reaches, or you reasonably expect it to reach, $75,000 in a rolling 12-month period (or $150,000 for not-for-profits), you must register for GST within 21 days. If you drive for taxi/limousine or ride-sourcing services, you must register from day one, regardless of turnover.

Once GST registration is done, you’ll need an ABN, charge 10% GST on taxable sales, lodge BAS on your chosen cycle, and you can claim GST credits on eligible purchases. To make this easier, use our Australian GST Calculator to quickly work out GST on sales and credits. Miss the window and the ATO can require you to back-pay GST from your “date of effect,” plus penalties and interest, so monitor turnover monthly and register early if you expect to exceed the threshold.

Do I need to register?

The threshold rule. You must have GST registration when your GST turnover reaches $75,000 (businesses) or $150,000 (not-for-profit). If you expect to cross the threshold, you should register; once you’re aware you’ll exceed it, you must do so within 21 days. Ride-sourcing & taxi/limousine = day one. Drivers providing taxi, limousine, or ride-sourcing services must register regardless of turnover; the threshold doesn’t apply.

“Expect to exceed” counts. The ATO assesses both current (this month + previous 11) and projected (this month + next 11) GST turnover on a rolling 12-month basis. If your pipeline/contracts mean you’ll reasonably exceed $75k, register now, don’t wait for the invoice to land. Edge case: one-off spike. If your current turnover has hit the threshold but your projected turnover for the coming 12 months does not, registration may not be required (exceptions still apply, e.g., taxi/ride-sourcing). Monitor monthly so you don’t miss the 21-day window.

How to calculate GST turnover

What “GST turnover” actually means. It’s your total business income (not profit), excluding GST, with several exclusions: input-taxed supplies (e.g., residential rent, many financial supplies), sales not connected with your enterprise, sales not connected with Australia, and other non-taxable receipts. In short: count taxable + GST-free supplies, exclude input-taxed/out-of-scope, and always work GST-exclusive.

Two tests you must run every month. Current GST turnover: this month + previous 11 months (rolling 12 months). Projected GST turnover: this month + next 11 months (rolling 12 months). If either hits the threshold ($75k; $150k for NFPs), you’re required to register. To make monitoring easier, you can use our Australian GST Calculator to work out GST amounts and stay compliant. Edge case to know. If your current turnover reaches the threshold but your projected turnover is below it, registration may not be required; keep monitoring monthly (ride-sourcing rules still override). This “current vs projected” carve-out comes straight from ATO guidance and the GST ACTs.

How to register (step-by-step)

Step 1: Log in to Online services for business

Go to Online services for business and sign in with myID (linked in RAM). From there, you can manage tax registrations for your ABN.

Step 2: Add GST to your ABN

Navigate to Profile → Tax registrations → Add/Update GST and follow the prompts. You can also register via Business.gov.au, by phone (13 28 66), or through your tax/BAS agent. Online services are the fastest.

Step 3: Set your “date of effect” (DOE)

Use the date you became required (or the date you choose if registering voluntarily). If you were required earlier, the ATO can backdate your registration, so choose this carefully.

Step 4: Choose your BAS reporting cycle

Monthly, if your GST turnover is $20 m+ (mandatory) or by choice, due the 21st of the following month. Quarterly by default if you’re < $20 m (unless the ATO tells you to report monthly). Annual only if you’re voluntarily registered and under $75k (or $150k NFP).

Step 5: Pick your GST accounting method

Cash basis: report when you receive/pay the money.

Non-cash (accruals): report when you issue/receive the invoice. Choose the method that matches your bookkeeping and cash flow; you can request a change later if eligible.

Step 6: Review & submit

Confirm contact and bank details, submit, and you’ll receive confirmation of registration. From then on, charge 10% GST on taxable sales, lodge BAS on your cycle, and claim credits where eligible.

Pick your BAS cycle & method

Choose your reporting cycle

Monthly, mandatory if your GST turnover ≥ $20 million (ATO may also direct some smaller businesses to report monthly). Due date: the 21st of the following month (e.g., July BAS → 21 August). Quarterly (default for most), if turnover is < $20 million and ATO hasn’t told you to report monthly. Due dates: 28 Oct, 28 Feb, 28 Apr, 28 Jul (often +2 weeks if lodging online). Annual, available only if you registered voluntarily (under $75k; $150k NFP). You lodge one annual GST return, due with your income tax return or by 28 February if no tax return.

Small-business perk: Simpler BAS (<$10 m)

If your GST turnover is < $10 million, you generally use Simpler BAS by default, report G1 (total sales), 1A (GST on sales), 1B (GST on purchases), and skip the rest. (Calculation rules don’t change; just fewer labels.)

Pick your accounting method (timing)

Cash basis, report GST when money is received/paid. Eligible if your aggregated turnover < $10 million (or if ATO allows). Helpful if customers pay late; GST hits when cash lands. Non-cash (accruals), report when you issue/receive the invoice (or part-payment), regardless of cash. Useful for larger ops or where accrual accounting is standard. Invoice $1,100 (incl. $100 GST) on 28 June; paid 5 July. On cash, you report the $100 on the July period; on accruals, you report it in June. (Same tax, different timing.)

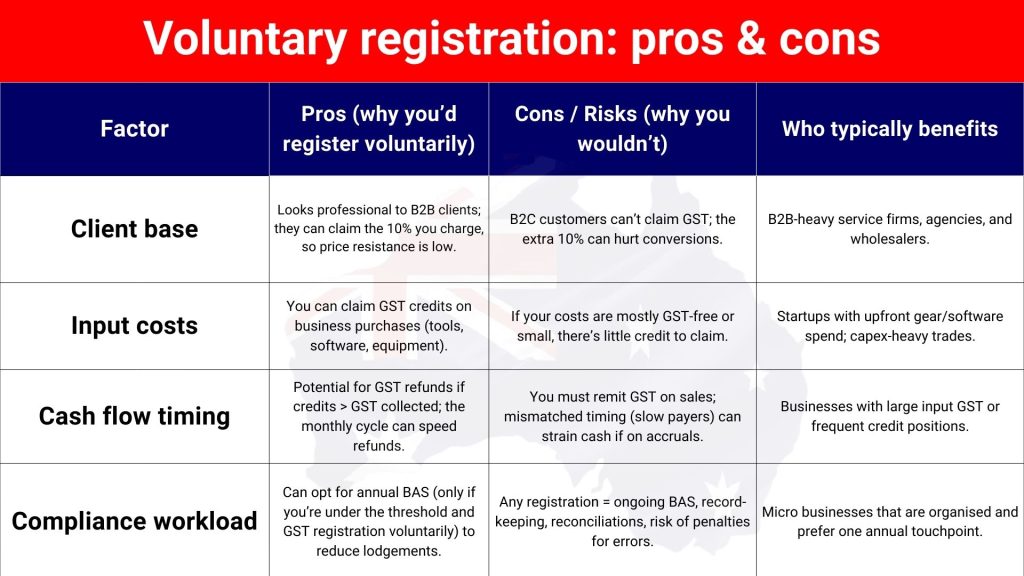

Voluntary registration: pros & cons

What if I’m late?

The ATO can backdate your GST registration to the day you became required (your “date of effect”). You’ll likely need to pay GST on past taxable sales, lodge the missed BAS returns, and you may be charged penalties and interest. Act fast; voluntary disclosure usually gets a better outcome.

What you’ll owe:

GST on past sales from your date of effect (even if you didn’t add GST on those invoices). Penalties/interest (often remittable in part if you disclose early and have good records).

What you can still claim:

GST credits on eligible business purchases from the same period (with valid tax invoices, business use, and within the normal claim time limits).

Conclusion

If you take nothing else away, take this: register the moment your GST registration turnover hits, or is clearly on track to hit,$75,000 (or $150,000 for NFPs) and do it within 21 days. That one move protects your cash flow and keeps the ATO off your back. From there, pick a BAS cycle that fits your size (monthly for the big guys, quarterly for most, annual only if you voluntarily registered under the threshold) and choose cash vs accruals based on how you actually get paid. Keep records tight, issue proper tax invoices, and claim credits you’re entitled to. Simpler BAS makes the admin lighter for small operators. Monitor turnover monthly and decide whether voluntary registration makes sense (great for B2B and input-heavy setups, not so hot for price-sensitive B2C). Ready to operationalise this? Run your next quote through the GST Calculator, set BAS reminders, and you’ll stay compliant without losing momentum.

Frequently Asked Questions (FAQs)

When do I have to register for GST?

Register when your GST turnover hits (or is expected to hit) $75,000 in any rolling 12 months ($150,000 for NFPs). You must register within 21 days of becoming required.

What exactly counts toward “GST turnover”?

It’s your business income excluding GST, assessed two ways: current turnover (this month + previous 11) and projected turnover (this month + next 11). Input-taxed sales and certain out-of-scope sales are excluded. If either test hits the threshold, you must register.

Do sole traders/freelancers need to register?

Yes, if your GST turnover meets the threshold or you reasonably expect to exceed it. If you’re under it, gst registration is optional (but brings BAS obligations).

I’m a rideshare/taxi driver, do I need to register even under $75k?

Yes. Taxi, limousine, and ride-sourcing providers must register from day one, regardless of turnover.